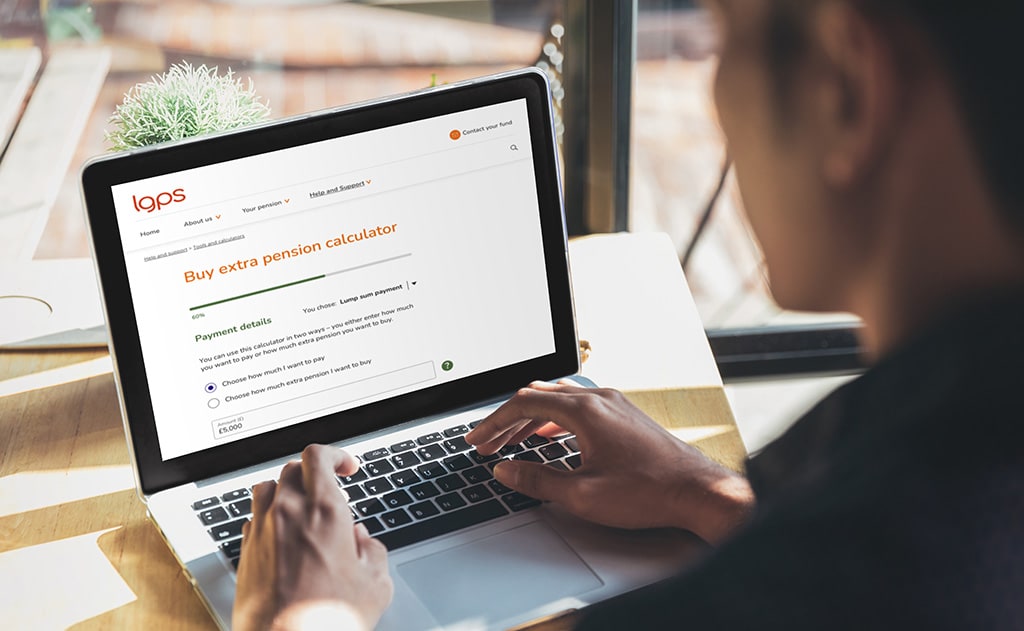

Try our calculators and tools

Our calculators and tools include:

More tools here…

Read our frequently asked questions to find out more about your pension

FAQs

Find out how the scheme is run and what to expect from your pension fund and employer

About the LGPS